Since the start of Russia’s full scale invasion of Ukraine, the Russian federal budget has received much more attention than in the past. For good reason: The budget can reveal a lot about the financial health and resilience of Vladimir Putin’s regime. It represents the flow of economic resources that is under formal, centralized control of the state.

When tax revenues are booming, as they did in the early months of the war, the federal budget can be used to cushion sanctions effects, pay for ramping up arms production, or to keep key elites happy. But when the revenue streams dry up, then a sickly budget can also become a real constraint for the regime. Despite being an autocrat, Putin cannot simply expropriate all savings or increase debt without limit (although both are happening to some degree). The risk of a major fallout becomes too great, even in a time of war.

Because of the political significance of the budget, the reliability of publicly available data is often questioned. In comparison to other autocracies, it may seem strange that Russia’s finance ministry is still publishing a lot of statistics. As of April 2023, it is still possible to get a relatively detailed and up-to-date picture of spending and revenues. Why is the Russian finance ministry not classifying all data? And how can we know whether the published numbers are made up?

There are several explanations that make Russia’s remaining data openness more plausible: First, deceiving the outside world about the actual state of affairs is not such a strong motive for Moscow as is sometimes assumed in the West. There is also relatively little censorship for economic debates within Russia, as long as they are wonkish enough to bore the public and the politics behind the numbers is not questioned. Second, for technocratic bureaucracies such as the finance ministry, transparency is a tool to strengthen and centralize control, both internally and vis-à-vis other actors in the government. More secrecy would eventually lead to more informal economic policy-making and more deals in the Kremlin’s backrooms, where the position of Russia’s technocrats is weaker. Keeping the numbers out in the public helps the technocrats to limit the influence of other elites that are always lurking in the shadows. Third, there is also inertia: In contrast to other autocracies such as China or Saudi Arabia, Russia went through a period of radical opening in the 1990s, and this process has not yet been fully reversed.

Available information and the confusion it creates

As of April 2023, Russia’s finance ministry is publishing almost daily updated data on revenues and — even more detailed — on expenditure through the Electronic Budget (budget.gov.ru). Access from outside Russia requires a VPN. Monthly statistics on oil and gas revenues are published early each month, followed by more data on expenditures and revenues around the middle of each month.

However, these budget numbers can be deceptive in the short run. Both revenues and spending always fluctuate strongly throughout the year, and since the start of Russia’s open war on Ukraine and sanctions against Russia’s economy, these fluctuations have intensified, which sometimes makes it hard to make out the underlying trends in the budget.

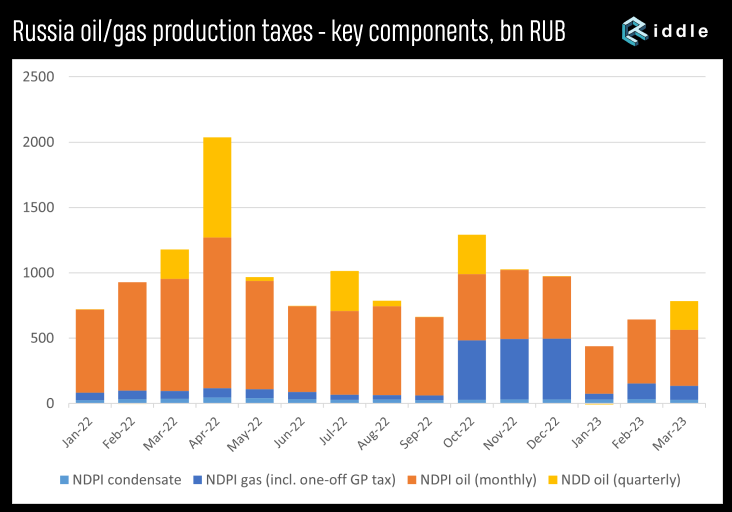

Even in normal times, both revenues and expenditures ebb and flow from month to month, obscuring the story behind monthly data. Revenue is inconsistent because tax payments are not even throughout the year, and because Russia is often changing its tax rules. For example, a newer oil production tax scheme («extra income tax», Nalog na Dopolnitel’nyy Dokhod, NDD) in combination with a gradual shift from export taxation to production taxation led to increased oil revenues in March, April, July and October — yet lower revenue in other months. At the same time, the reimbursement of VAT payments was accelerated in 2022, leading to lower VAT revenue early each quarter. Russia also fundamentally amended its tax payment procedures and timelines in January 2023, causing additional noise in the data. All of these changes led to temporarily smaller revenues in January and February 2023. Of course, special measures linked to the war and the economic crisis can also have strong temporary effects, such as last year’s one-off tax on Gazprom which led to significant extra revenue in late 2022.

Expenditures fluctuate according to a spending cycle that is somewhat typical in many public budgets and institutions: Spending in December is usually twice as high as in other months. In December 2022, this phenomenon was particularly strong, with 22% of Russian total 2022 expenditure accruing in that month. This spike was indirectly related to the new tax payment procedures, which made an advance payment to the social security fund necessary. The war has also led to more irregular accumulation of spending in some periods.

The Russian finance ministry helps to interpret the data by publishing a few paragraphs of explanations with the monthly budget numbers. Interviews with officials can also offer extra hints about what is going on under the hood of the budget. But these official explanations need to be taken with a grain of salt. While they are not factually wrong, they sometimes don’t tell the whole story.

A partial explanation for the weak start of the year

In early 2023, Russia’s state finances seem to be in bad shape. In February, the deficit already reached 2.6 trillion RUB, which is 88% of the originally planned full-year deficit of 2.9 trillion RUB. In March, the deficit shrank to 2.4 trillion thanks to the aforementioned quarterly «extra income tax» on oil producers and higher VAT revenue due to the end of the quarter; but the shortfall after three months still looks too high.

If you zoom out from the monthly data to the full year, there are reasons to believe that the low revenue from oil and gas in the first three months of 2023 (45% below last year) will be temporary. That is because sanctions have distorted the finance ministry’s tax rates, which led to lower tax revenue (and slightly happier Russian oil exporters). Since the EU embargo on Russian crude was introduced, price indices for Russian Urals oil have become very unreliable. To calculate tax rates, Russia’s finance ministry is still using a Urals index provided by the pricing service Argus, which is based on reported transactions in European ports. According to the finance ministry, the monthly average of this index was close to 50 USD / barrel between December 2022 and March 2023. Actually, the oil companies were making much more money than that: A recent study based on detailed Russian customs data has shown that Russian exporters were still earning over 70 USD / barrel in December 2022.

Of course, the Russian finance ministry is aware of this and plans to get its share. Since April 2023, a new formula for oil taxation is in force: If the difference between Urals and Brent prices becomes too large, the Brent index will be used, minus a certain pre-defined discount (34 USD in April, 31 USD in May, 28 USD in June, 25 USD in July, see. This will alleviate some of the revenue shortfalls that hurt the budget in January and February, alongside revenue from the «extra income tax» in March and April.

Secret expenditures are driving the deficit

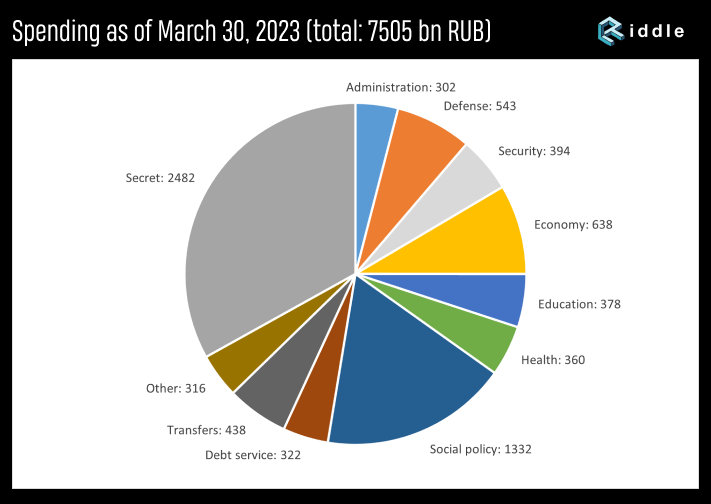

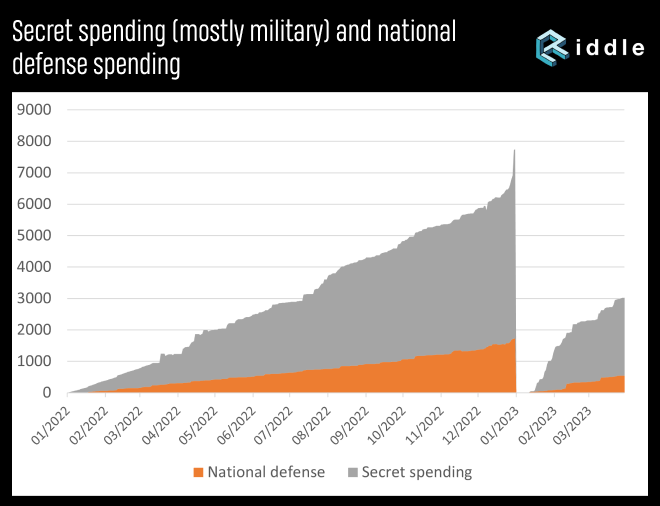

While the revenue was below expectations (both due to the EU oil embargo and lower global oil prices), the bigger surprise (and the main reason for the deficit) was the drastic increase in spending early in the year. Most notably, secret spending was much higher than last year; it was 33% of all spending. Secret spending can be calculated by deducting the spending shown across different budget categories in the Electronic Budget from total spending on the same day. In early April, the Electronic Budget showed total spending around 7.5 trillion RUB, while secret (unexplained) spending stood at 2.5 trillion RUB. That is more than twice as much as last year: At the same time in 2022, secret spending was just around 1 trillion RUB.

* Secret spending data from January to March 2022 is a linear extrapolation due to incomplete information in the Electronic Budget

Usually, 80% of secret spending is defense expenditure and another 10% goes to national security expenditure. The biggest item in secret spending is always the state arms programme. Since Russia’s open invasion of Ukraine, any increase in secret spending is likely war-related. But does the increase stand for a sustainable trend or is it a one-time effect?

To justify the abnormally high spending in January 2023, the Russian finance ministry explained that some state contractors received higher advance payments to achieve a more even spending throughout the year. Prime minister Mishustin explained how the intention was to «put the money to work starting first of January». The high share of secret spending suggests this is indeed about state contracts: more precisely, weapons for the war. In fact, the growth of secret spending (and spending overall) slowed in March 2023.

The more plausible explanation, however, is not some kind of technocratic optimization of spending flows as the finance ministry claims, but simply that the arms industry and the military need more cash up front to expand and sustain production, and the finance ministry is adjusting spending on the fly. After all, the president promised «unlimited funding» to the army late last year.

Partly to preempt ad-hoc war demands, the finance ministry has created a few invisible piggy banks for this year’s budget, the biggest being an advance transfer of 1.5 trillion rubles (1% of GDP) to Russia’s social security fund in late 2022. The finance ministry was worried that the fund would run into a liquidity problem due to new tax payment procedures set in January 2023. In theory, this advance payment should lead to smaller transfers needed in 2023, and as of March, the category of social spending is indeed 13% below 2022 figures.

It appears as if the finance ministry itself cannot really forecast how much spending will be demanded by the war this year, and it simply set a low total spending guideline and a few hidden reserves into what will be a lot of bargaining and upwards revisions. The security apparatus and the military, on the other hand, can ignore the budgetary limits for now and rest assured that their wishes will be fulfilled and funds will be allocated when the time comes.

All of this explains why the finance ministry’s reassurances that current advance payments lead to less spending later in 2023 come with one big caveat: Most likely, there even more advance payments for even more warfare later on. In other words: «We are spending earlier this year» is most likely just a delicate way of saying «We are spending much more».

The outlook: Unsustainable, but not yet critical

So the nature of Russia’s wartime budget is unpredictable (or in the words of the finance ministry: flexible). Nevertheless, a few conclusions can be drawn: Some of the negative effects that led to high deficits in January and February 2023 will be reversed later in the year. This is particularly true with the size of revenues, which could still reach the planned 26.1 trillion RUB. VAT revenue will normalize; oil revenue meanwhile will rise due to its seasonal fluctuations, helped by the weak ruble and higher tax rates (which are a stronger factor than Russia’s 5% cut in oil production, particularly after other nations in OPEC+ joined in). The government could also intensify its efforts to generate a larger budget by leaning on wealthy businessmen. The windfall tax planned for this year will generate just 300 billion rubles, which is equivalent to an oil price increase of 2 dollars; yet businessmen could also be enlisted directly, i.e. to cover expenses of reconstruction in occupied territories.

However, all of these efforts will not bring ongoing budget spending back in line with the framework set in the 2023 budget, making upwards revisions necessary. The 29.9 trillion RUB total spending foreseen according to the latest Electronic Budget would still mean that Russia spends significantly less than in 2022 in nominal terms, despite a jump in inflation and a presidential election coming up in early 2024. This is simply not plausible. After a budget shortfall of 2.3% of GDP in 2022, most analysts expect the deficit somewhere between 3% and 5% this year, instead of the official forecast of 2%.

For the Russian state, which does not have access to Western capital markets anymore (and is unable to get access to the Chinese capital market so far), an annual deficit of 3−4% of GDP is quite significant and hardly sustainable in the longer run, despite the low overall level of debt. The problem is not (yet) skyrocketing interest payments, but the question of how to finance the added deficit. The finance ministry has two main options: Emptying the National Welfare Fund or issuing more local debt. According to the finance ministry, the liquid part of the Welfare Fund currently stands a little over 6.4 trillion RUB or 4% of GDP. Although the weaker ruble helps the liquid part (mainly in Western currencies) of the fund to last longer, it will be exhausted sometime in 2024 at currrent rates, forcing the finance ministry to rely exclusively on borrowing.

All roads lead to inflation

Economically, it does not make a big difference if the ministry exhausts the fund or borrows more. This is because the finance ministry cannot sell most of its «liquid» assets in the Welfare Fund on the open market (due to sanctions). Instead, the Central Bank takes them and credits the finance ministry with rubles to spend. Emptying the welfare fund is thus mostly an internal transaction of the Russian government that increases money supply, except for relatively insignificant sales of Chinese yuan that are mandated by Russia’s budget rule (only 10% of Welfare Fund spending). Regarding the effect on money supply in Russia, the effects of issuing new bonds are actually quite similar.

This means that both emptying the National Welfare Fund and issuing debt puts upwards pressure on inflation, which will at some point threaten the paradigm of macroeconomic stability that Putin has adhered to throughout his time in power. That paradigm change is still a couple of years away: Central bank governor Elvira Nabiullina still appears to have the mandate to tame inflation in Russia by raising interest rates. So far, the Russian market and the population still believe that inflation will be contained, and that the monetary authorities are in control, simply because that’s how it was in the last two decades.

But in a country at war, principles such as central bank independence usually don’t hold up, just as the finance ministry will not be able to return to fiscal prudence. As Russia’s economy struggles under Western sanctions and labor shortages caused by the war and outmigration, Nabiullina should expect increasing headwinds if she adds to the pain by raising interest rates. It also pits the central bank against the finance ministry, because fighting inflation will make it more difficult for the state to borrow. The discussions around the need for fighting inflation may have already begun.

The outlook of Russia’s fiscal and monetary foundations is still relatively stable as of today. However, once the trust in the central bank is eroded, and Russians adjust their individual expectations about the ruble’s stability, the situation could change quicker than Russia’s economic resilience in 2022 may suggest.